Often times users in SAP are puzzled by why a certain vendor’s invoices are not selected by the payment run.

We will discuss one reason that is easy to identify and resolve.

When running a payment proposal SAP blocks the vendors whose invoices have been selected in another proposal. The savvy user will check the payment proposal log where he will be able to see vendors that are blocked by another proposal.

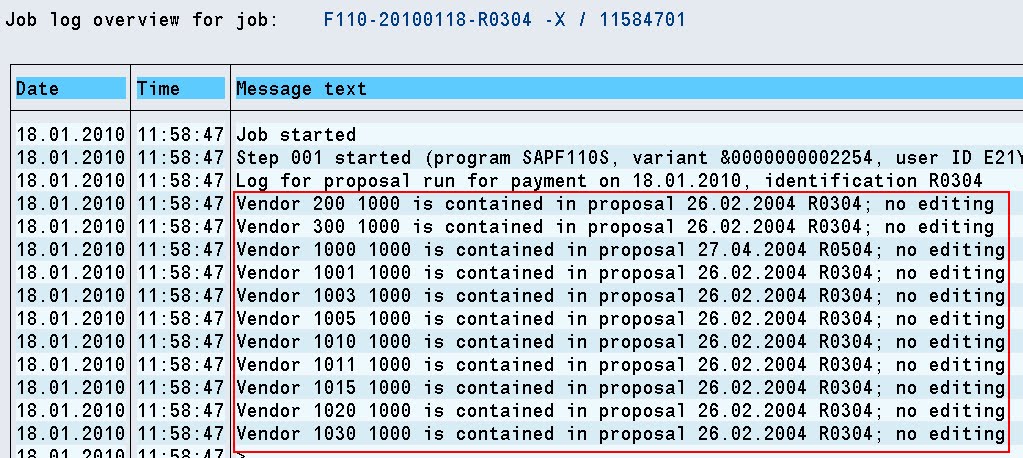

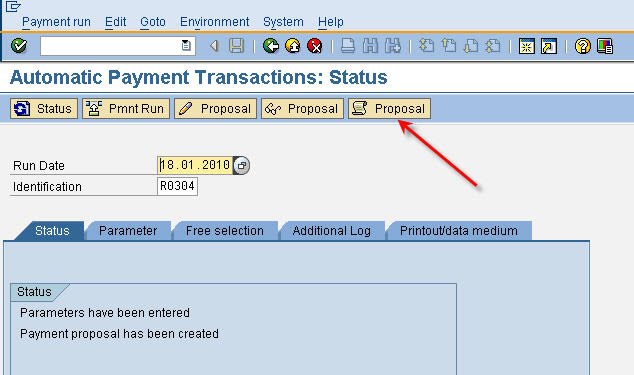

In this case I have run a proposal on the 18th but for some reason vendor 1000’s invoices are not showing up. By pressing the proposal log button from within the payment run, Figure 1, the proposal log will be displayed, Figure 2. When examining the log, I will easily see that, that vendor 1000 is contained in a different proposal. At this point I have two options, either complete the other proposal or delete it to release the blocked invoices.

But what if you want to see all the vendors that are blocked by different proposals not just the ones that have been selected for payment in a specific proposal.

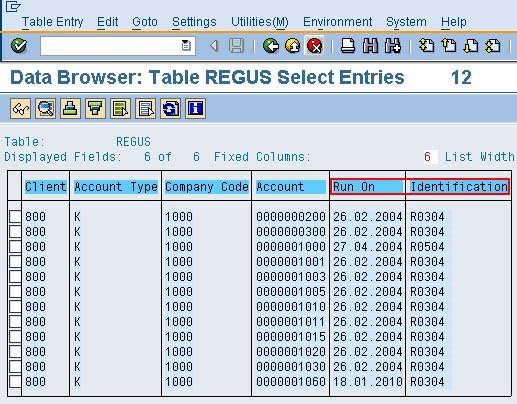

In this case you can query table REGUS: Accounts blocked by payment proposal

By querying the different rows in this table you will be able to obtain a listing of all the vendors that have been blocked in a proposal. Figure 3 displays the output of table REGUS.

By reviewing the contents of this table you will be able to see the “Run On” and Identification” fields required for finding the payment proposals that are blocking payment to your vendors.